Commercial Gaming Revenue Tracker

May 2026 Commercial gaming Revenue Tracker

The American Gaming Association’s (AGA) Commercial Gaming Revenue Tracker features state-by-state and nationwide financial performance data with breakdowns for individual gaming verticals.

TOPLINE INDUSTRY TRENDS

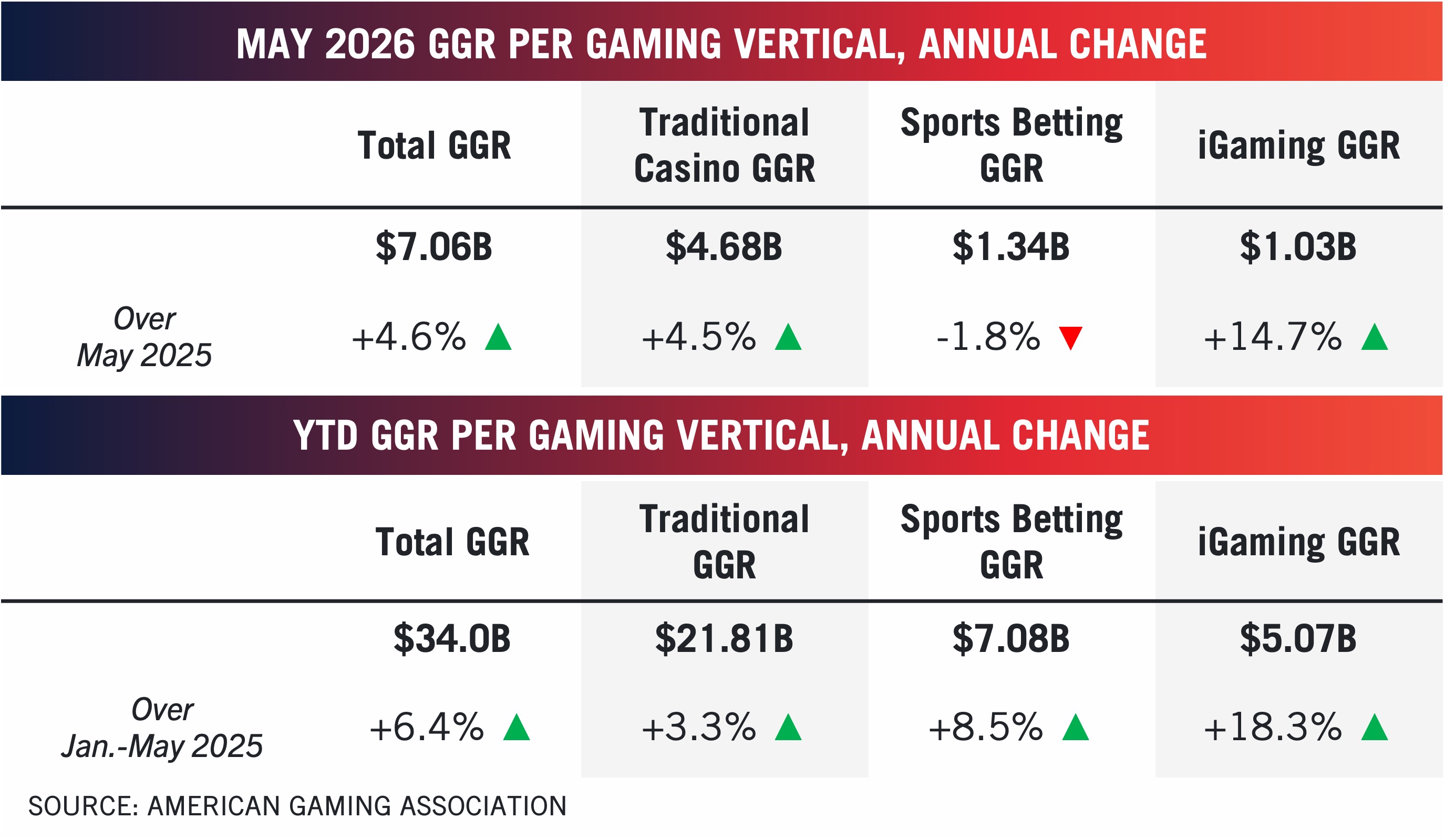

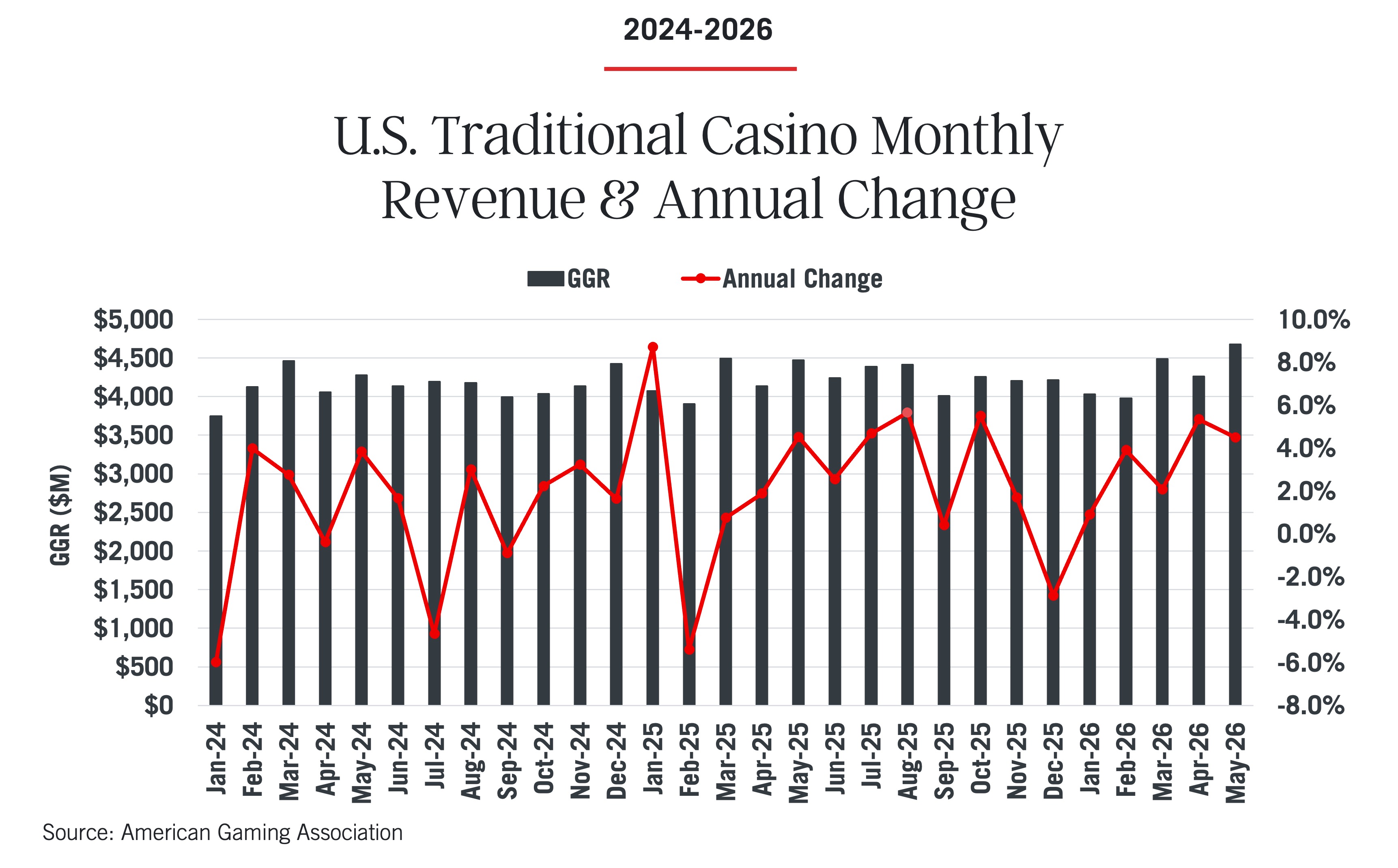

Strong Growth Across All Verticals: U.S. commercial gaming revenue grew 4.6 percent in May driven by strong brick-and-mortar casino performance as legal sports betting revenue and state gaming taxes declined in the face of expanded backdoor prediction market competition.

![]()

Traditional casino gaming expanded by 4.5 percent to $4.68 billion.

- Slot machines generated $3.39 billion (+4.6%)

- Table games revenue generated $933 million (+3.9%)

$3.39 Billion

generated by slot machines in May 2026.

$933 Million

generated by table games in May 2026.

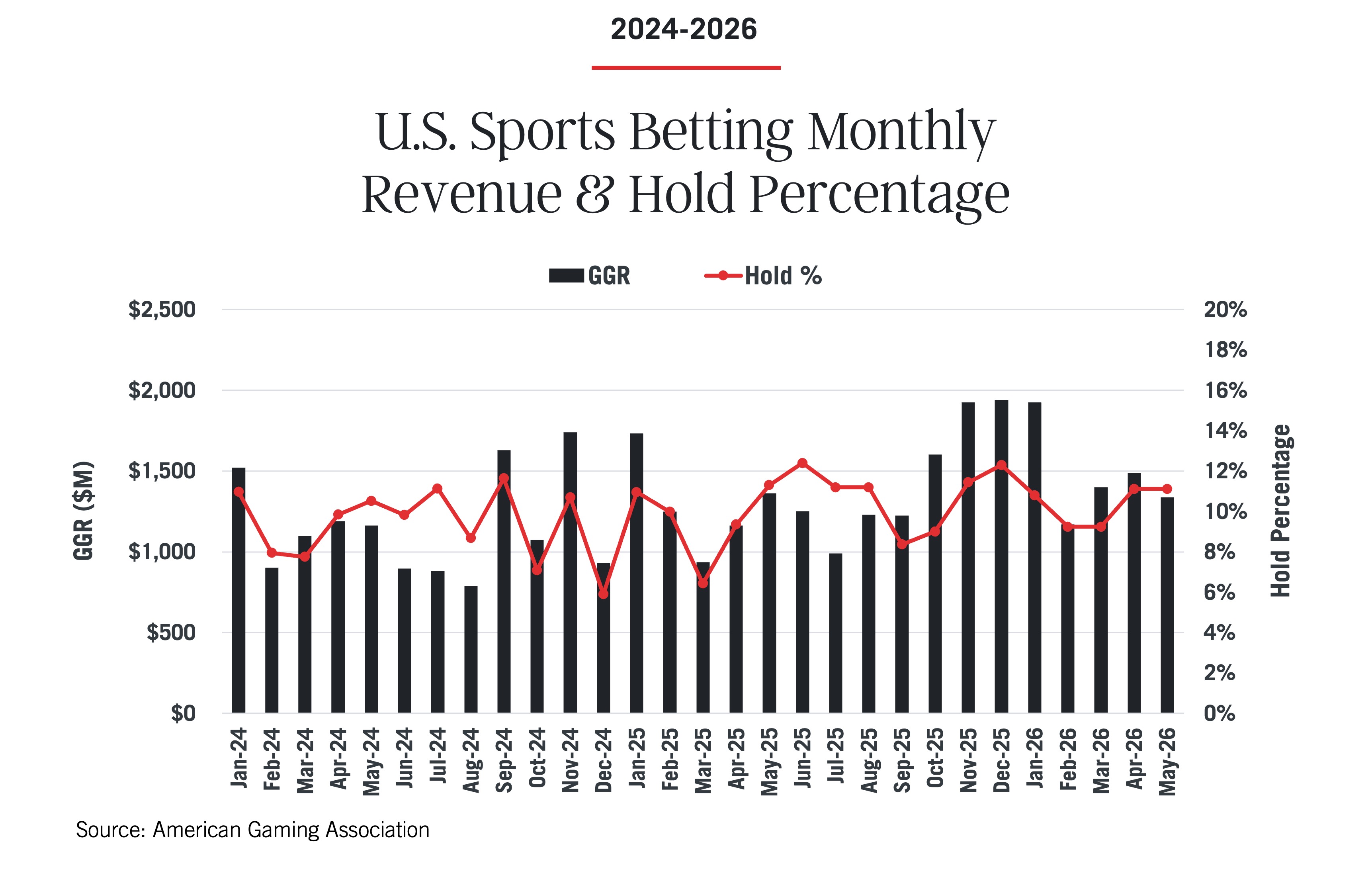

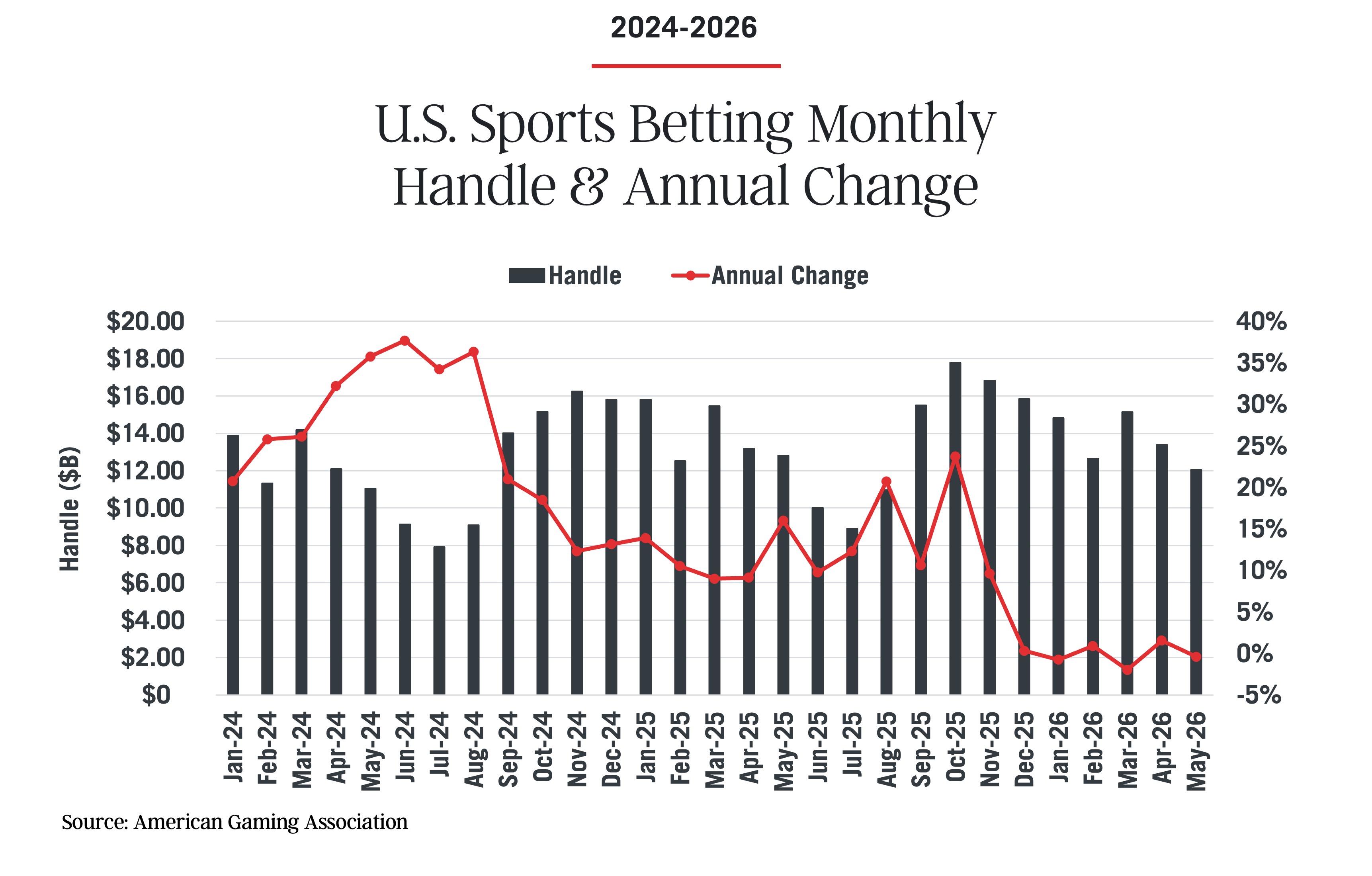

Sports betting revenue fell 1.8 percent in May to $1.34 billion on handle of $12.06 billion (-0.4%).

Sports betting revenue contracted for the second month this year, driven by declining handle and lower hold, which fell 16 basis points from last May. Excluding the new market of Missouri, handle fell 2.7 percent as sports betting on prediction markets continues to explode outside of state regulatory guardrails.

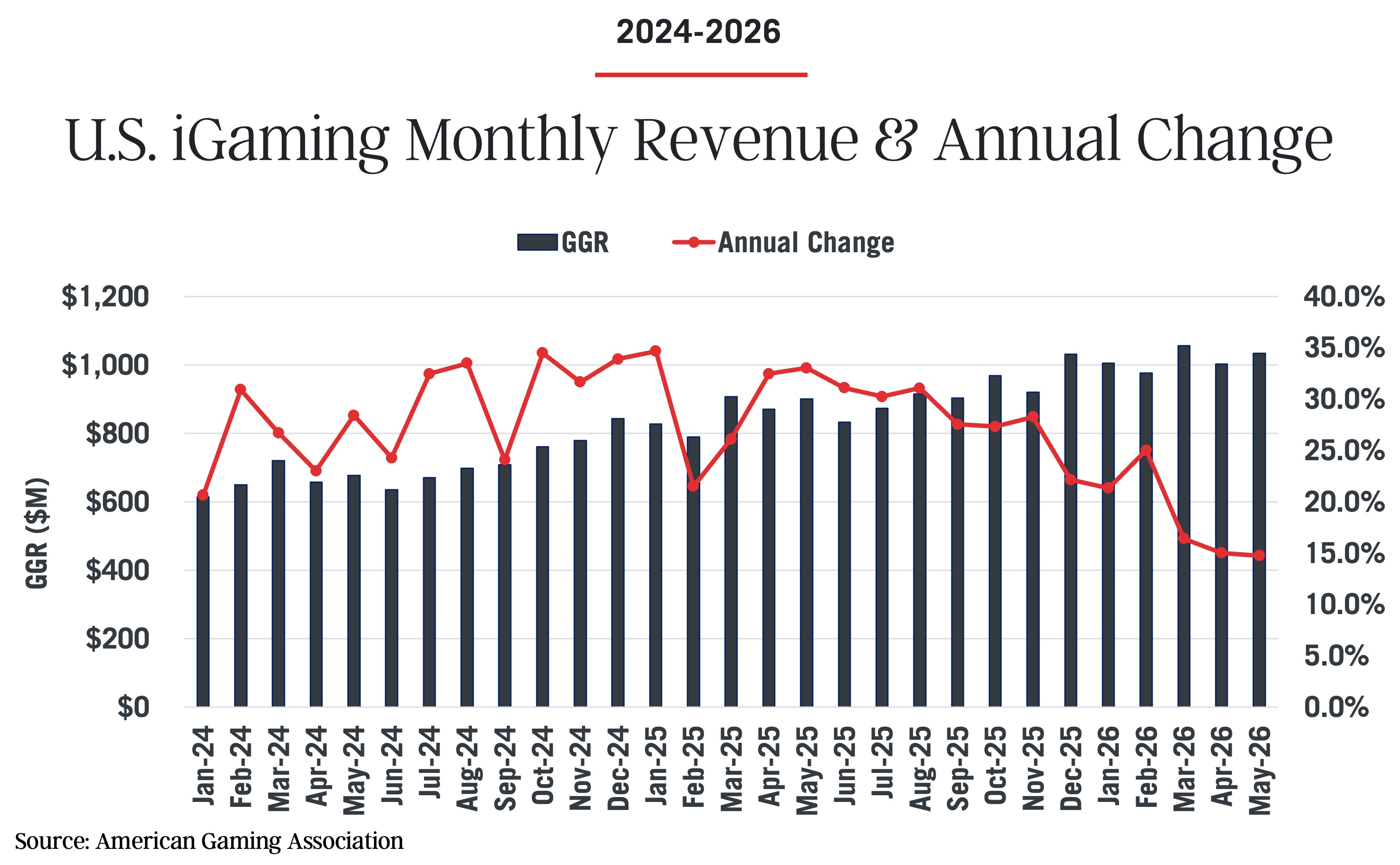

iGaming generated $1.03 billion in May revenue, a 14.7 percent increase compared to the previous year. While iGaming continues to be the fastest growing segment of the U.S. market, with no new markets coming online since 2024, the pace of growth has slowed significantly over the last few months.

State Budget Impacts: Regulated gaming generated $1.53 billion in gaming tax revenue for vital state programs for May, up marginally from last year (0.7%). This figure could be significantly higher but is impacted by operators of skill machines, “sweepstakes casinos” and those offering illegal sports bets through prediction market platforms, none of which pay state gaming taxes.

State sports betting tax revenue fell 2.4 percent in May as state-regulated handle and revenue declined while Kalshi alone handled nearly $15 billion in sports betting volume.

Prediction market platforms offering sports bets have cost state governments over an estimated billion dollars in potential gaming taxes since the start of 2025, depriving seniors’ pension plans and responsible gaming programs, among other victims, of critical funding.