State of the States 2023

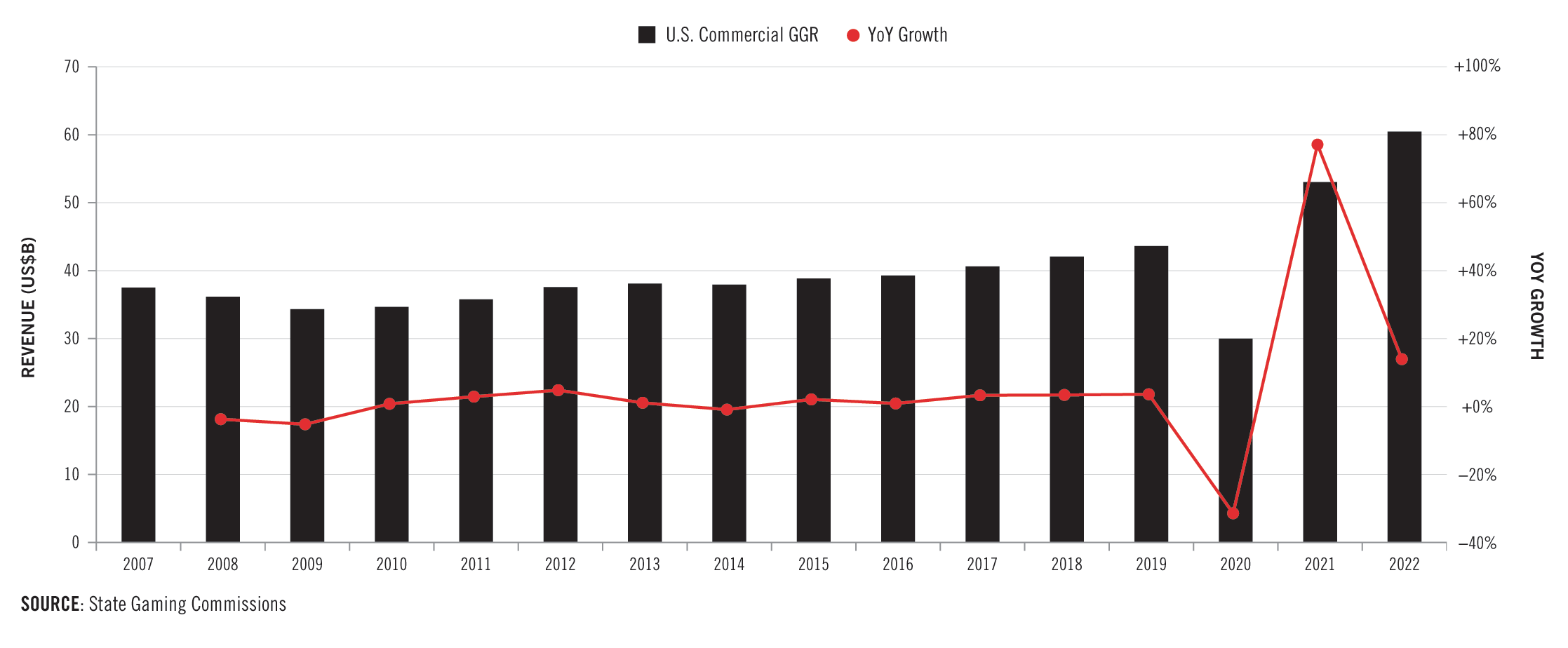

Despite persistent concerns about the financial health of American consumers throughout 2022, the U.S. commercial casino gaming industry generated record-breaking revenue for a second consecutive year as total nationwide consumer spending on commercial casino gaming and sports betting increased by 14.0 percent to $60.46 billion.

Annual U.S. Commercial Gaming Revenue

Key Findings

“As one of the biggest taxpayers in states across the country, we know that when gaming is successful, so are our communities. Beyond our significant tax contributions, our industry is ingrained in local communities, bolstering economic development through job creation, supporting local charities and nonprofits, and setting the standard on corporate responsibility." - AGA President And CEO Bill Miller

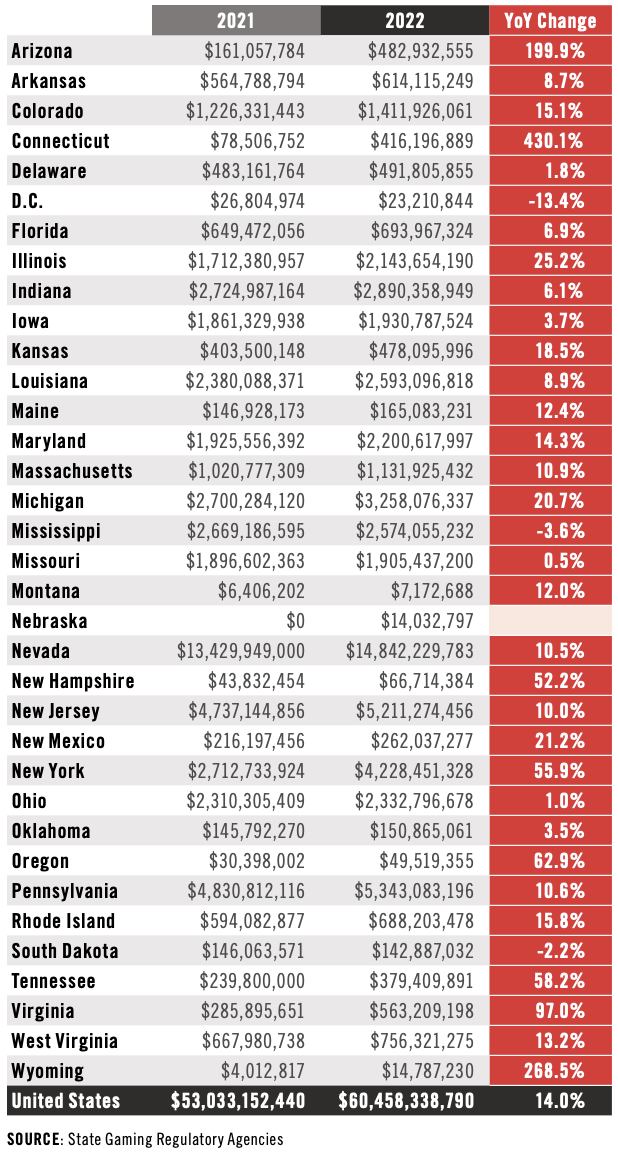

In 2022, nearly all of the 35 jurisdictions with commercial casinos or sports betting operations saw a rise in annual gaming revenue, with only the District of Columbia, Mississippi and South Dakota reporting a decline. Twenty-seven out of the 35 jurisdictions achieved their highest-ever annual revenue from commercial gaming. Notably, Nebraska and Virginia joined the commercial casino marketplace in 2022 with the expansion of land-based casinos into each state.

Commercial Casino Gaming Consumer Spend by State 2021 vs. 2022

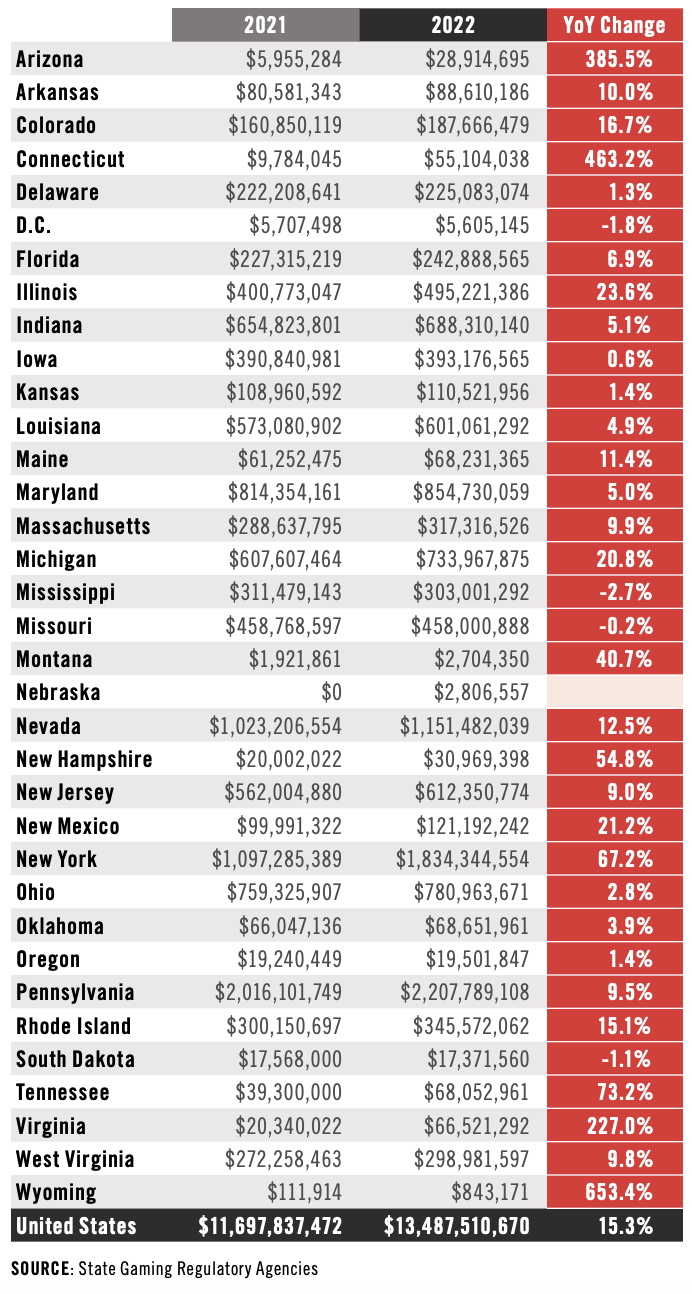

The surge in gaming revenue resulted in an unprecedented $13.49 billion of direct gaming tax revenue disbursed to state and local governments by commercial gaming establishments, reflecting a 15.3 percent increase compared to 2021. This figure just includes specific state and local taxes directly linked to gaming activities. The $13.49 billion does not encompass the billions of dollars paid by the industry in the form of income taxes, sales taxes or various corporate taxes, nor does it incorporate the payroll taxes paid by gaming operators and suppliers. Federal excise tax payments made by sports betting operators are also excluded from the total.

Commercial Casino Direct Gaming Tax Revenue by State 2021 vs 2022

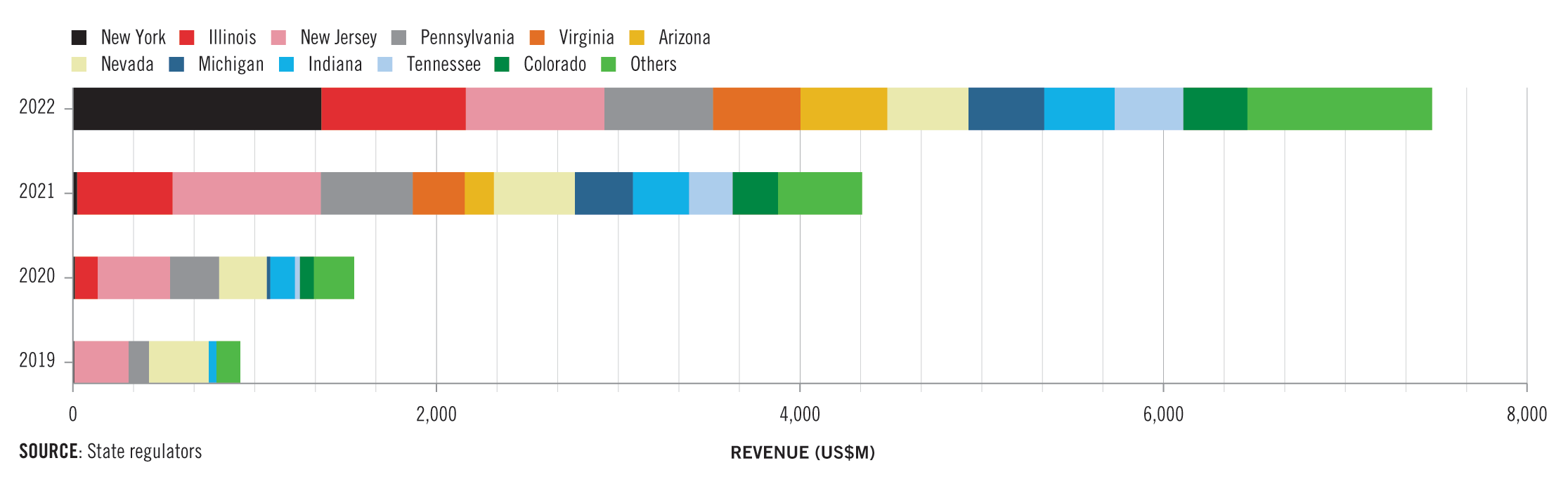

While land-based gaming still dominated the overall commercial gaming revenue pie, sports betting and iGaming saw tremendous growth in 2022, setting new annual records.

Sports betting revenue soared 61.1 percent year-over-year, from $4.34 billion in 2021 to $7.50 billion in 2022, as Americans bet a total of $93.2 billion on sports throughout the year. The growth was driven by the launch of legal betting in Kansas and the addition of mobile betting in Louisiana, Maryland and New York.

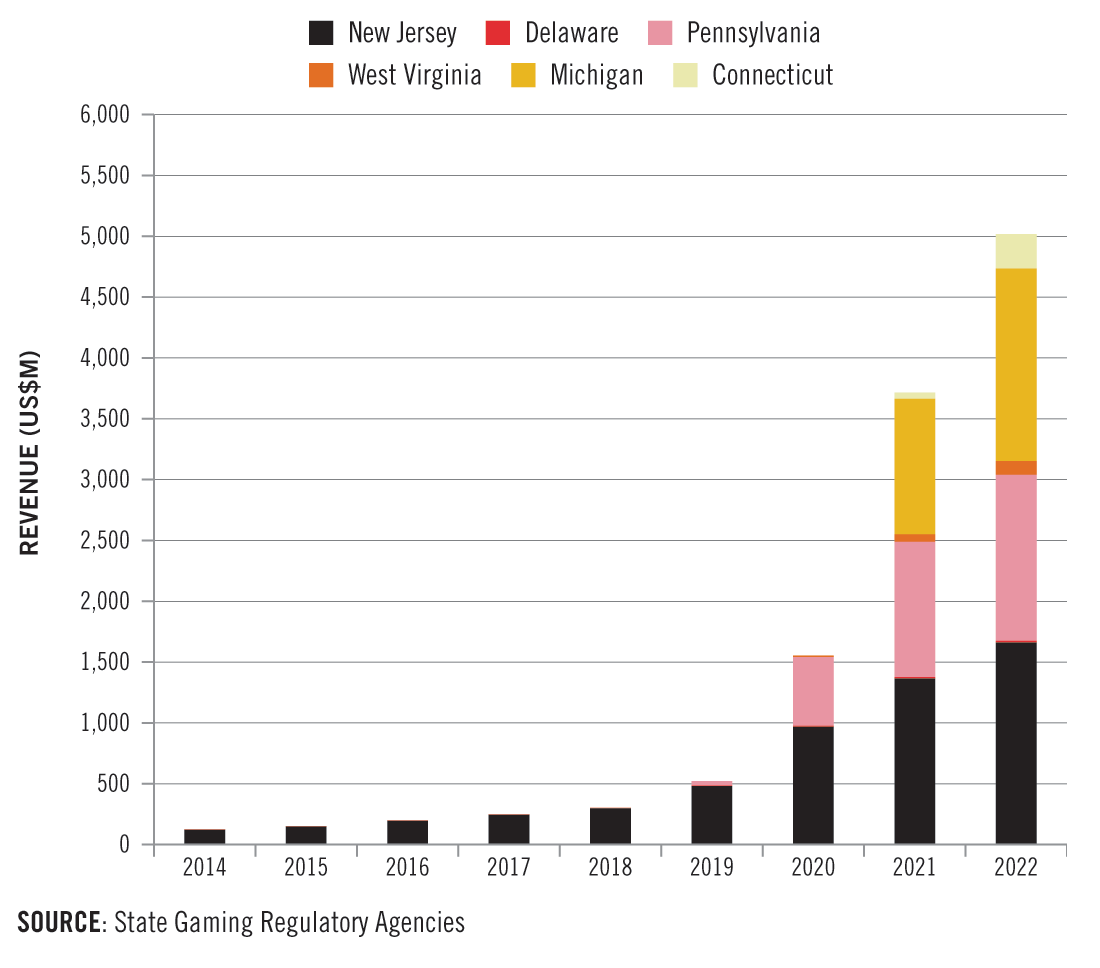

The geographically smaller iGaming market also continued to break records in 2022, with combined iGaming revenue from six active states (excluding Nevada’s online poker only market) reaching $5.02 billion, a 35.2 percent increase year-over-year. Notably, iGaming’s growth came without any new states launching in 2022.

United States: Regulated Sports Betting GGR (US$BN) – 2019 to 2022

United States: Regulated iGaming GGR – 2014 to 2022

About State of the States

AGA’s annual State of the States report details the commercial gaming industry’s financial performance, including analyses of each of the 35 jurisdictions with commercial gaming operations in 2022. The report, developed with VIXIO GamblingCompliance, also provides a breakdown of the legality of types of gaming and number of casinos by state, summarizes major gaming policy discussions, and previews opportunities and challenges for the industry. The companion State of Play map provides the report findings, as well as key regulatory and statutory requirements for each state, in an easy-to-use, interactive tool.