Gaming Industry Outlook

Gaming Industry Outlook: Prediction Market Concerns Increase

Real economic activity in the gaming industry continued to expand and executive outlook remained strong, though prediction markets have begun to impact business, according to the American Gaming Association’s Gaming Industry Outlook.

More than 60% of AGA member executives expect increased capital investment, boosted revenues, and improved balance sheet health over the next six to 12 months.

The positive outlook comes amidst economic and competitive threats. Inflation continues to put pressure on company margins and consumer spending, with the conflict in the Middle East and higher gas prices exacerbating these issues. As executives continue to adjust to the changing economic environment, reduced hiring remains the norm, and wage pressure on margins remain a central concern for operations.

Prediction markets also emerged as a growing threat – 81% of executives view these markets as a very significant threat to the regulated gaming industry.

The Gaming Industry Outlook provides a snapshot of the industry’s current and future economic health based on executive sentiment, gaming activity and economic indicators.

Key highlights include the following:

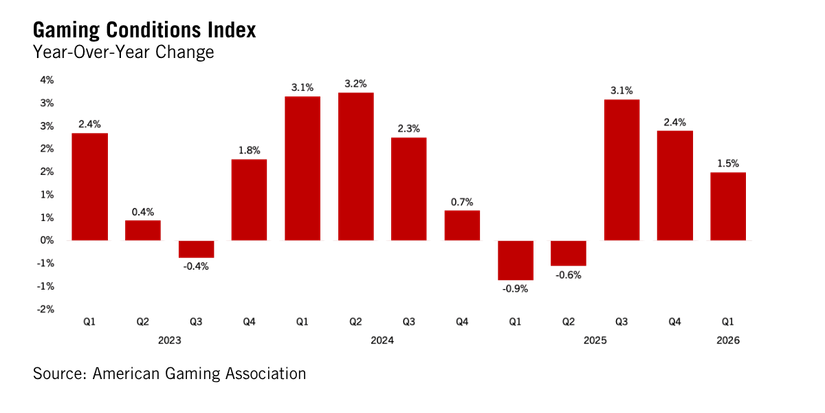

- The Gaming Conditions Index (GCI or the Index) shows economic activity in the industry growing in Q1 2026 compared to the prior year. The Index tracks real economic activity in the sector, measured by gaming revenue, employment, employee wages and salaries, gaming executive sentiment, and future event activity at casino hotels.

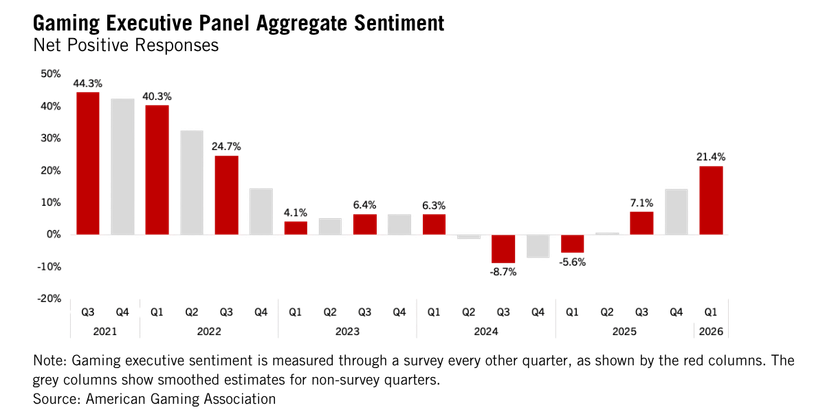

- Gaming executive sentiment was largely positive, with the highest positive response rate since Q3 2022. More respondents gave positive responses (e.g., “expect increase”) than negative ones (e.g., “expect decrease”) across a range of questions pertaining to factors such as business situation, revenue growth and customer activity.

Gaming Conditions Index

The GCI indicates real economic activity in the industry, as measured by gaming revenue, employment, employee wages and salaries, executive sentiment and casino hotel event activity, increased 1.5% in Q1 2026 relative to the prior year. This continues the expansion seen in the previous two quarters, driven by positive executive sentiment.

Executive Sentiment

Gaming executive sentiment grew to 21.4% net positive, highest since Q3 2022. Respondents’ outlook improved across a range of questions pertaining to factors such as business situation, revenue growth and customer activity. For context, because the aggregate sentiment measure is greater than zero, it means that there was a higher number of positive responses compared to negative responses. Sentiment was particularly strong around expected revenue growth, customer activity, overall business situation and capital investment.

Economic Outlook

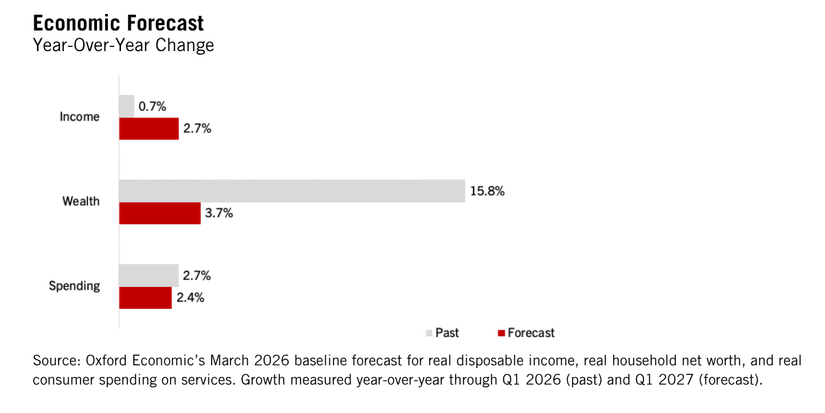

Despite continued uncertainty, the U.S. economy is expected to remain resilient, benefiting from investment in AI and other industries. Oxford Economics’ March forecast anticipates the continuation of the “k-shaped” economy, with building pressure on lower-income households due to increased prices from the conflict in the Middle East. Higher-income households, benefiting from tax cuts, are expected to keep consumer spending on services positive (2.7% in Q1 2026; 2.4% in Q1 2027). Strong growth in household wealth (15.8% in Q1 2026; 3.7% in Q1 2027) is likely to have a positive tailwind effect on consumer spending as well. Continued growth is also expected in real disposable income (0.7% in Q1 2026; 2.7% in Q1 2027).

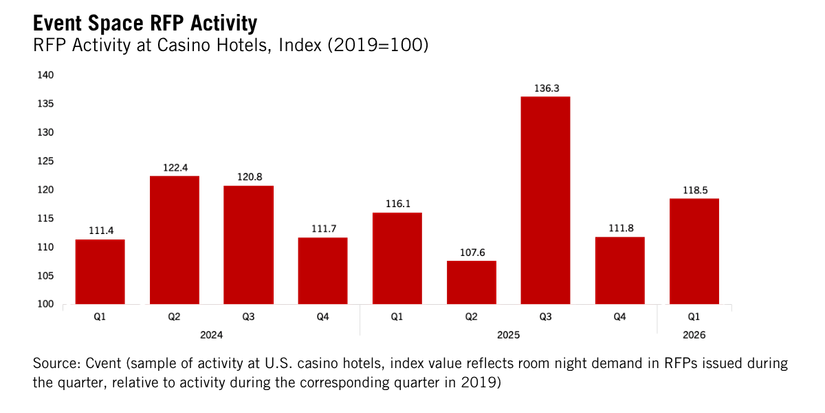

Casino Hotel Event Activity

Casino hotels continue to receive RFPs for events, such as business meetings and social events, at a pace that’s above pre-pandemic levels. Relative to a year ago, the number of RFPs received has increased by 2%, indicating a continued appetite for booking events at casino hotels.

Gaming Executive Panel Highlights

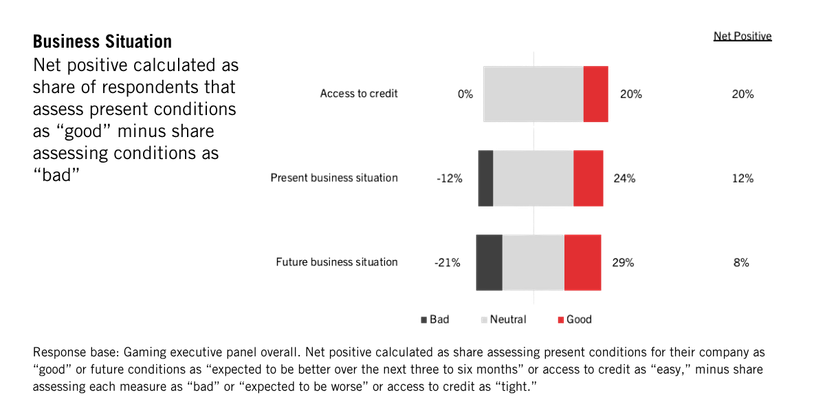

Executive sentiment remained positive in Q1 2026. Gaming executives’ views on the current business situation improved slightly to 12% net positive in Q1 2026 (24% positive, 64% neutral, 12% negative) from 11% net positive in Q3 2025.

When asked about the future business situation, 29% of executives expected improvement, while 21% expected deterioration. This 8% net positive is significantly lower than the 26% net positive reported in Q3 2025 but still indicates favorable conditions. Executive near-term outlook reached record highs in several key business areas.

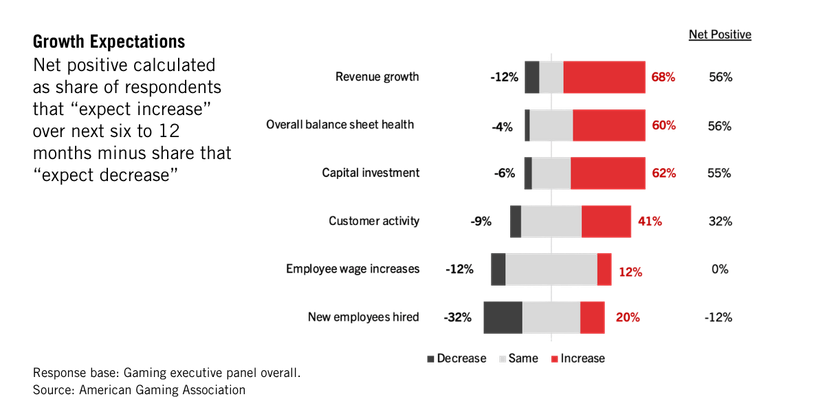

Executives indicated strong growth expectations around revenue (56% net positive), overall balance sheet health (56% net positive), and customer activity (32% net positive). The implementation of AI is also expected to benefit the gaming industry, with 50% of executives expecting cost savings in the next six to 12 months.

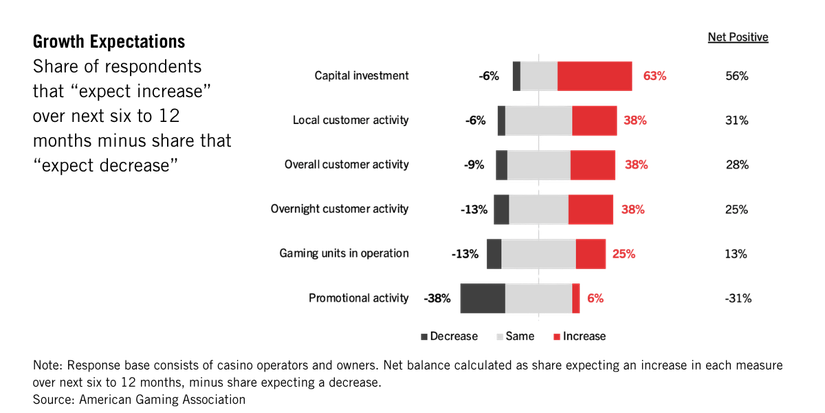

Gaming executives continue to plan for capital investment, with 62% of respondents indicating increased capital investment over the next six to 12 months. Additionally, promotional activity is expected to continue to decline, as executives expect a decrease in promotional activity for the second consecutive quarter (31% net negative).

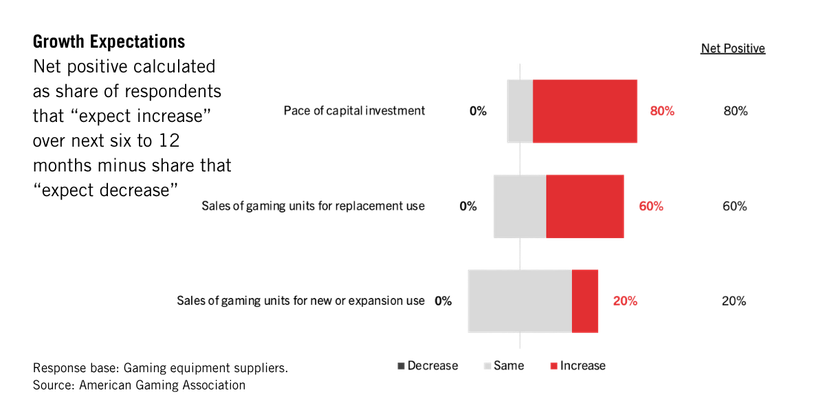

Among gaming equipment suppliers, sentiment remained positive, with strong expectations around the pace of capital investment and the sale of gaming units for new, expansion, or replacement use. Since the beginning of the survey, expectations around capital investment among gaming suppliers have never been stronger (55% net positive).

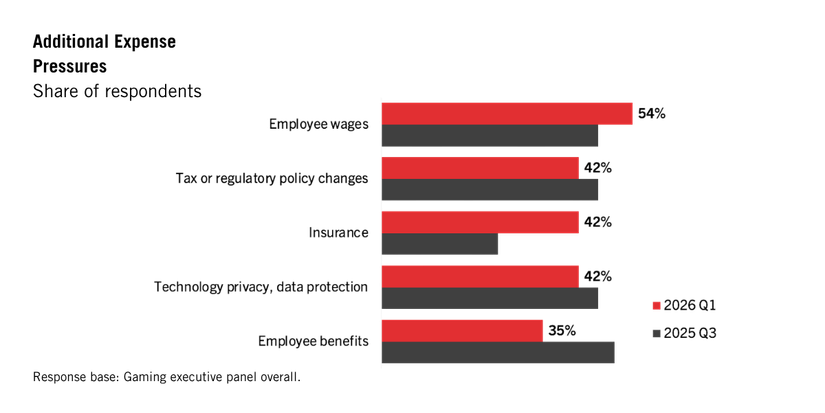

Industry hiring expectations continued to stall, as executives indicated negative expectations for the seventh consecutive survey. When asked to identify expense pressures, the highest share of executives selected employee wages (54% of respondents).

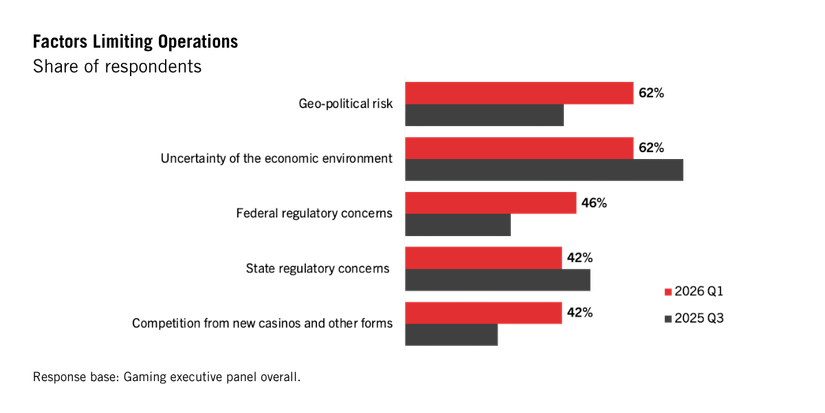

Economic and political uncertainty continues to be a concern for executives, with tariffs, inflation, and geopolitical conflict putting increasing pressure on supply chains.

Prediction markets were also cited by 81% of executives as a “very significant” threat to the gaming industry and 46% of executives now indicate that federal regulatory concerns are limiting operations, up from 29% in Q3 2025. Additionally, 42% of executives cite competition from new forms of gaming as a major factor limiting operations, up from 25% last fall.

Sentiment around the current and future business situation remains positive.

Expected revenue growth and balance sheet health continue to be a bright spot for gaming executives.

Expectations around customer activity growth remain high, while capital investment expectations increase dramatically.

Outlook around supplier sales expectations and expected pace of capital investment vastly improve.

Regulations around prediction markets are seen as a top priority for gaming executives.

Short answer comments by executives on aspects of operations requiring greater than normal levels of management attention included the following examples:

Prediction Markets

“Unregulated and untaxed competition;” “Threat of further expansion into gaming markets;” “Impact industry credibility.”

Technology

“AI integration;” “Technology system upgrades;” “Cybersecurity.”

Economic Conditions

“Managing labor expenses;” “Rising supply chain costs;” “Tariffs;” “Tightening consumer budgets.”

Economic and political uncertainty are the top factors limiting operations.

Employee wages, taxes and regulatory changes pressure margins.